If you’re turning 65 or already on Medicare, one of the biggest questions you’ll run into is this:

“What’s the difference between Medicare Advantage and Medicare Supplement plans?”

And honestly, it’s a good question — because the names sound similar, but the plans work very differently.

As a Medicare agent here in New York, I talk to people on Long Island every day who feel overwhelmed trying to figure it all out. One commercial says Medicare Advantage gives you “everything you need.” Another person tells you to get a Supplement plan. Then someone else says, “Don’t forget Part D!”

It’s confusing. And unfortunately, a lot of people enroll in plans without fully understanding how they work until they actually need medical care.

So let’s break this down in plain English.

This article will help you understand:

- what Original Medicare covers

- how Medicare Advantage works

- how Medicare Supplement (Medigap) works

- the biggest pros and cons of each

- and which option may make more sense depending on your health, lifestyle, and budget here on Long Island.

First: What Is Original Medicare?

Before comparing anything else, it’s important to understand the foundation.

Original Medicare includes:

- Medicare Part A (hospital coverage)

- Medicare Part B (medical coverage)

Original Medicare is provided by the federal government.

It covers many medically necessary services, but it does not cover everything. In fact, one of the biggest surprises for many people is learning that Original Medicare generally leaves you responsible for:

- deductibles

- copays

- coinsurance

- and 20% of outpatient medical costs with no maximum out-of-pocket limit.

That’s where Medicare Advantage and Medicare Supplement plans come in.

Both are designed to help fill gaps in Medicare — but they do it in completely different ways.

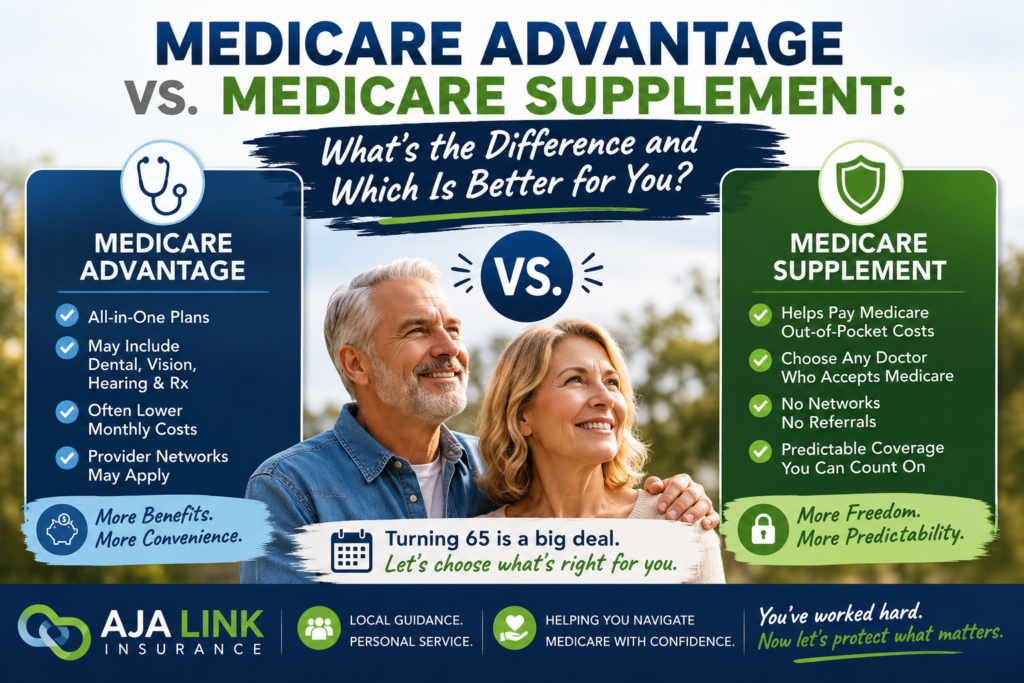

What Is a Medicare Supplement Plan?

A Medicare Supplement plan — also called Medigap — works alongside Original Medicare.

Instead of replacing Medicare, it helps pay many of the costs Medicare doesn’t fully cover.

For example:

- hospital deductibles

- skilled nursing facility copays

- the 20% coinsurance under Part B

- copays and other out-of-pocket expenses depending on the plan.

These plans are designed to help reduce the medical costs that Original Medicare doesn’t fully pay on its own.

These plans are standardized by the government.

That means:

- a Plan G from one company provides the same basic coverage as a Plan G from another company.

The main differences are usually:

- monthly premium

- customer service

- rate history

- and company reputation.

How Medicare Supplement Plans Work

With a Supplement plan:

- Medicare pays first

- Your Supplement plan pays second

One of the biggest reasons people choose Medigap is freedom.

With most Supplement plans, you can:

- see any doctor nationwide who accepts Medicare

- avoid most referrals

- travel more easily

- and have predictable medical costs.

This is especially important for many Long Island retirees who:

- travel seasonally,

- see specialists in Manhattan,

- or want flexibility with provider access.

Popular Medicare Supplement Plans in New York

In New York, the most common plans people compare are:

- Plan G

- High Deductible Plan G

- Plan N

Many people like Supplement plans because they provide peace of mind and predictable coverage.

What Is Medicare Advantage?

Medicare Advantage plans are different.

Instead of supplementing Medicare, these plans actually replace the way you receive your Medicare benefits.

Medicare Advantage plans are offered by private insurance companies approved by Medicare.

These plans bundle:

- Part A

- Part B

- and usually Part D prescription coverage.

Many also include extra benefits like:

- dental

- vision

- hearing

- gym memberships

- over-the-counter allowances

- transportation

- and more.

This is why Medicare Advantage commercials are everywhere.

The plans often look attractive because:

- some have low premiums,

- some are $0 premium plans,

- and they include extra benefits Original Medicare doesn’t cover.

It’s simply a different way of receiving your Medicare benefits, and understanding how the plan works is the key to deciding whether it’s the right fit for your needs.

The Biggest Difference: Networks

One of the most important differences between Medicare Advantage and Medicare Supplement is provider access.

Medicare Supplement

With a Supplement plan:

- you can generally see any doctor nationwide who accepts Medicare.

No network restrictions in most cases.

This is a huge benefit for people who:

- travel often

- want specialist flexibility

- or don’t want to worry about referrals.

Medicare Advantage

Medicare Advantage plans usually use:

- HMO networks

- PPO networks

- or EPO-style networks.

That means:

- you may need to stay in-network,

- you may need referrals,

- and certain services may require prior authorization.

This doesn’t mean Medicare Advantage is bad.

It simply means it’s important to understand how the plan works before enrolling.

On Long Island especially, provider networks matter a lot because many people use:

- Northwell

- NYU Langone

- Mount Sinai

- Stony Brook

- Memorial Sloan Kettering

- and specialty physician groups.

Not every plan works with every doctor or hospital system.

Costs: Which Is Cheaper?

This is probably the biggest question people ask.

The answer depends on:

- your health

- your medical usage

- and how comfortable you are with risk.

Medicare Supplement Costs

Supplement plans usually have:

- higher monthly premiums

- but lower out-of-pocket costs when you use care.

Many people like knowing:

“If I get sick, my costs are still predictable.”

Medicare Advantage Costs

Medicare Advantage plans often have:

- lower monthly premiums

- but higher pay-as-you-go costs when services are used.

You may have:

- copays

- coinsurance

- hospital day costs

- specialist visit costs

- imaging costs

- and maximum out-of-pocket exposure.

Some years you may spend very little.

Other years can become much more expensive if your health changes.

Prescription Drug Coverage

Another big difference:

Medicare Supplement

Prescription coverage is NOT included.

You usually need:

- a standalone Part D drug plan.

Medicare Advantage

Most plans already include Part D coverage.

That convenience appeals to many people.

Which Plan Is Better?

Honestly?

There is no universal “best” choice.

The right plan depends on the individual.

That’s why it’s important to work with a trusted Medicare agent who can help you compare your options based on your doctors, prescriptions, budget, and healthcare needs. Medicare Advantage and Medicare Supplement plans work very differently, and having someone guide you through the pros and cons can make the decision feel much less overwhelming.

Medicare Supplement May Be Better If:

- you travel often

- you want nationwide flexibility

- you see specialists frequently

- you dislike referrals or prior authorizations

- you want more predictable costs

- you can comfortably afford higher monthly premiums

Medicare Advantage May Be Better If:

- you are relatively healthy

- you prefer lower monthly costs

- your doctors are in-network

- you’re comfortable using provider networks

- you want extra benefits like dental or vision

- you don’t mind copays when using services

Important New York Medicare Rules

New York is unique when it comes to Medicare Supplement plans.

New York has something called:

Guaranteed Issue/Open Enrollment Year-Round

This means many people in New York can switch Medicare Supplement plans without medical underwriting.

That’s a major advantage compared to many other states.

However, timing and eligibility still matter, so it’s important to speak with a licensed Medicare professional before making changes.

The Mistake Many People Make

One of the biggest mistakes people make is focusing only on:

- premium

- commercials

- or extra benefits.

Instead, people should focus on:

- provider access

- prescription coverage

- total out-of-pocket risk

- and how they actually use healthcare.

A $0 premium plan may sound amazing — until someone discovers their doctor isn’t in-network or they need expensive treatment later.

At the same time, paying for a high-premium Supplement plan may not make sense for everyone either.

That’s why personalized guidance matters.

Final Thoughts

Choosing between Medicare Advantage and Medicare Supplement is one of the biggest Medicare decisions you’ll make.

And the truth is:

the right answer is different for everyone.

Some Long Island retirees love the flexibility and predictability of Supplement plans.

Others are perfectly happy with Medicare Advantage and appreciate the lower premiums and extra benefits.

The key is understanding:

- how the plans work,

- what your financial comfort level is,

- and whether your doctors, hospitals, and medications are covered.

Medicare can feel overwhelming at first, but it becomes much easier once someone explains it clearly and honestly.

If you have questions about your Medicare options in New York or on Long Island, it’s always a good idea to speak with a licensed Medicare professional who can walk through your specific situation and help you compare plans carefully.